Indecision Costs

Indecision Costs

|

|

More money has been lost to indecision than was ever lost to making the wrong decision. The economy and the housing market have caused some people to take a “wait and see” position that could cost them in lost opportunities as well as almost certain higher costs in the future.

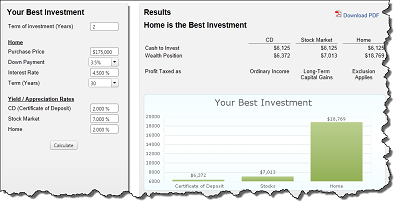

To illustrate what the opportunity cost might be, let’s compare what the value of the down payment two years from now would be if it was invested in a certificate of deposit, the stock market or used to purchase a home today.

A 3.5% down payment on a $175,000 home is $6,125.00. If it was invested in a CD that would earn 2%, a person would have $6,372 in two years. The earnings would be taxed as ordinary income tax rates. It wouldn't earn much but it would be safe and secure.

The same amount would grow to $7,013 in the stock market if you picked the right stock or fund and it yielded 7%. The earnings would be taxed at the long term capital gains rate. The return could be greater but so is the risk involved.

If this person were to purchase a home today that appreciated 2% in value over the next two years, the equity in the home would grow to $18,769 due to value going up and the unpaid balance going down.

|

|

The question, we all must ask ourselves is “where should our money be invested?” Try Your Best Investment to see the difference it will make based on your price range, down payment and earning rate.