One Size Doesn't Fit All...

One Size Doesn't Fit All

Rarely, does one size fit everyone and the same goes for advice. The following suggestion is not right for everyone. However, for people with job security and who don't own a home; for people with good credit and enough savings for a down payment, there may never be a better time to buy a home.

|

|

Homes have had a significant price correction but in many markest, they have started to rise again. The lower prices combined with historically low interest rates make this an opportune time to buy a home if you can afford it.

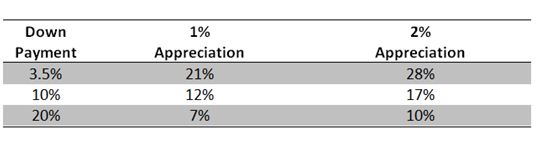

One of the reasons homes are an attractive investment is that fact that you can use a small down payment and finance the balance for 30 years. The principle, called leverage, allows you to earn a return on the value of the home rather than the actual cash investment. Small appreciation can create a large rate of return on the initial investment of the down payment and closing costs.

The following example is a projection at the end of five years for a $175,000 home with 3% closing costs and a 5% interest rate for a 30 year term. The rate you see in each column is an annual rate of return based on the equity of the home at the end of the five year period due to both appreciation and amortization of the loan.

The nature of positive leverage will cause the returns to be higher with a smaller down payment. As you see in the table, the return is higher on the 3.5% down payment than with the 10% or 20% down payment.

If you're curious to see if this advice might fit your situation, you really need to sit down with a knowledgeable real estate professional who can help you assess your position. It's worth the time because there may never be a better opportunity than now.