Finding the Best Mortgage

As rates are inching up but still very affordable, buyers should remember that there is an alternative to a fixed rate mortgage that can provide the lowest cost of housing for the homeowners who understand the parameters.

|

|

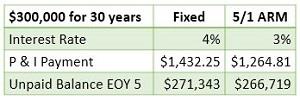

A $300,000 fixed-rate mortgage at 4% has a principal and interest payment of $1,432.25 per month for the entire 30 year term. A 5/1 adjustable mortgage at 3% has a $167.43 lower payment for the first five years and then, can adjust, up or down, based on a predetermined index.

Another interesting fact is that the unpaid balance on the ARM at the end of the first five years is $4,624 lower than the fixed-rate mortgage. The total savings in the first five years on the ARM is $14,669.00.

Adjustable rate mortgages are not the right choice for everyone but buyers should at least consider the options based on their individual situation. It could be an obvious choice for a buyer who is only going to be in the home for five years or less.

Use the ARM Comparison worksheet to see what possible savings you could have based on your actual numbers. A trusted mortgage professional can help you to understand the advantages and disadvantages based on your situation. You need the facts to make the best decision.