Shopping for a Mortgage

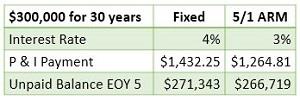

A lower rate will not only result in a lower payment, it will amortize the loan quicker. A $250,000 mortgage at 4.5% for 30 years will have a $1,266.71 principal and interest payment. At 4%, the same loan will have $1,193.54 payment saving $73.18 a month and the unpaid balance would be $1,776 lower at the end of five years.

Mortgage lenders tend to price their mortgages based on the credit score of the borrower. The higher the credit score, the lower the mortgage rate. There is an inverse relationship that the lower the credit score, the higher risk and therefore, a higher rate is needed to balance the risk.

In order to get a valid rate that will be available to you with your credit score, you need to be pre-approved. The process of making a loan application before you find a home, allows the lender to verify your credit, income, and ability to repay the loan. Lenders usually only charge the cost of the credit report for this type of service. Be aware that pre-approval is not the same thing as pre-qualification which is simply a loan officer's opinion.

When you shop for a mortgage with multiple lenders, the credit bureaus count them as a single credit inquiry if they are done within a two-week period. On the other hand, restrain yourself from applying for other credit such as cars, furniture or credit cards until after you have closed on the purchase of your home because those inquiries can negatively affect your credit score.

The Consumer Financial Protection Bureau recommends that you let lenders know that you are shopping the mortgage for the best rate and fees.

Instead of going to the Internet and Googling mortgage lenders, start with recommendations for a lender from your real estate professional. They see the good, the bad and the ugly and can save you a lot of time. Another reliable source would be from a friend who has recently purchased a home.

There are lenders who bait unsuspecting borrowers with lower rates and fees into making an application and after critical time has lapsed, try to switch them to a different program. By that point, many buyers feel they don't have any choice but to accept what is offered.

Another confusing factor is the way that loans are priced to the public. They are usually quoted at a rate with a certain amount of points. A point is one percent of the amount borrowed. An example would be a quote for a loan at 4.5% with 1 point or at 4% with 2.5 points.

The points combined with the rate affect the yield the lender will earn, and you will pay. A simple way to make this an apple to apple comparison is to have the lender quote the loan as a "par-value" loan with no points involved. Then, the lowest rate will produce the lowest cost to you.

Another way to compare loans will be to uses a financial app called Will Points Make a Difference. You can plug in the rate and points to calculate the lowest yield over a projected holding period or the full term.

The lenders do not want to make it easy for you to compare. Mortgage money is a commodity and shopping will be worth the effort.

There is much more than a lower rate and payment to determine whether to refinance a mortgage. Lenders try to make refinancing as attractive as possible by rolling the closing costs into the new mortgage so there isn't any out of pocket cash required.

There is much more than a lower rate and payment to determine whether to refinance a mortgage. Lenders try to make refinancing as attractive as possible by rolling the closing costs into the new mortgage so there isn't any out of pocket cash required.