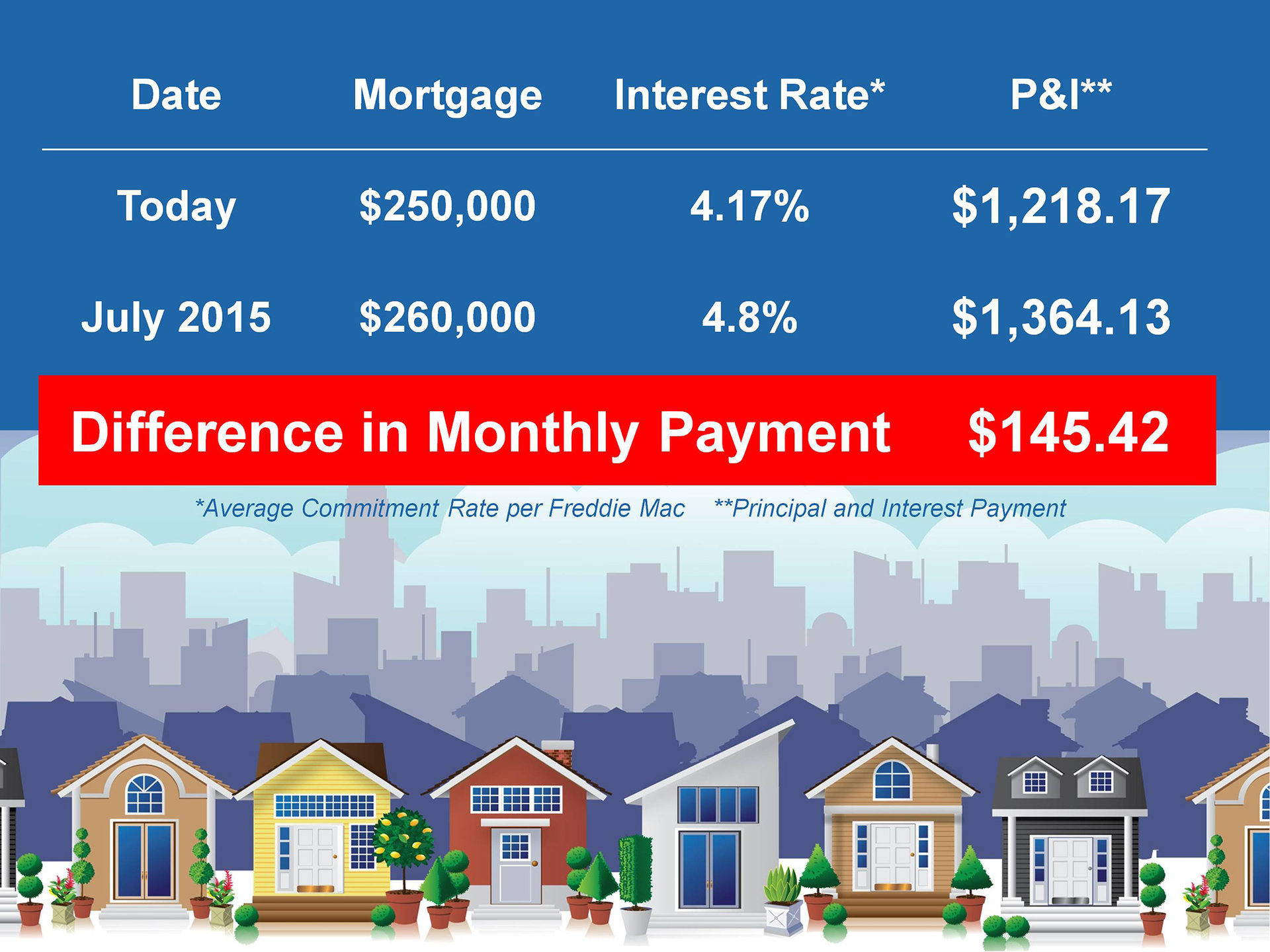

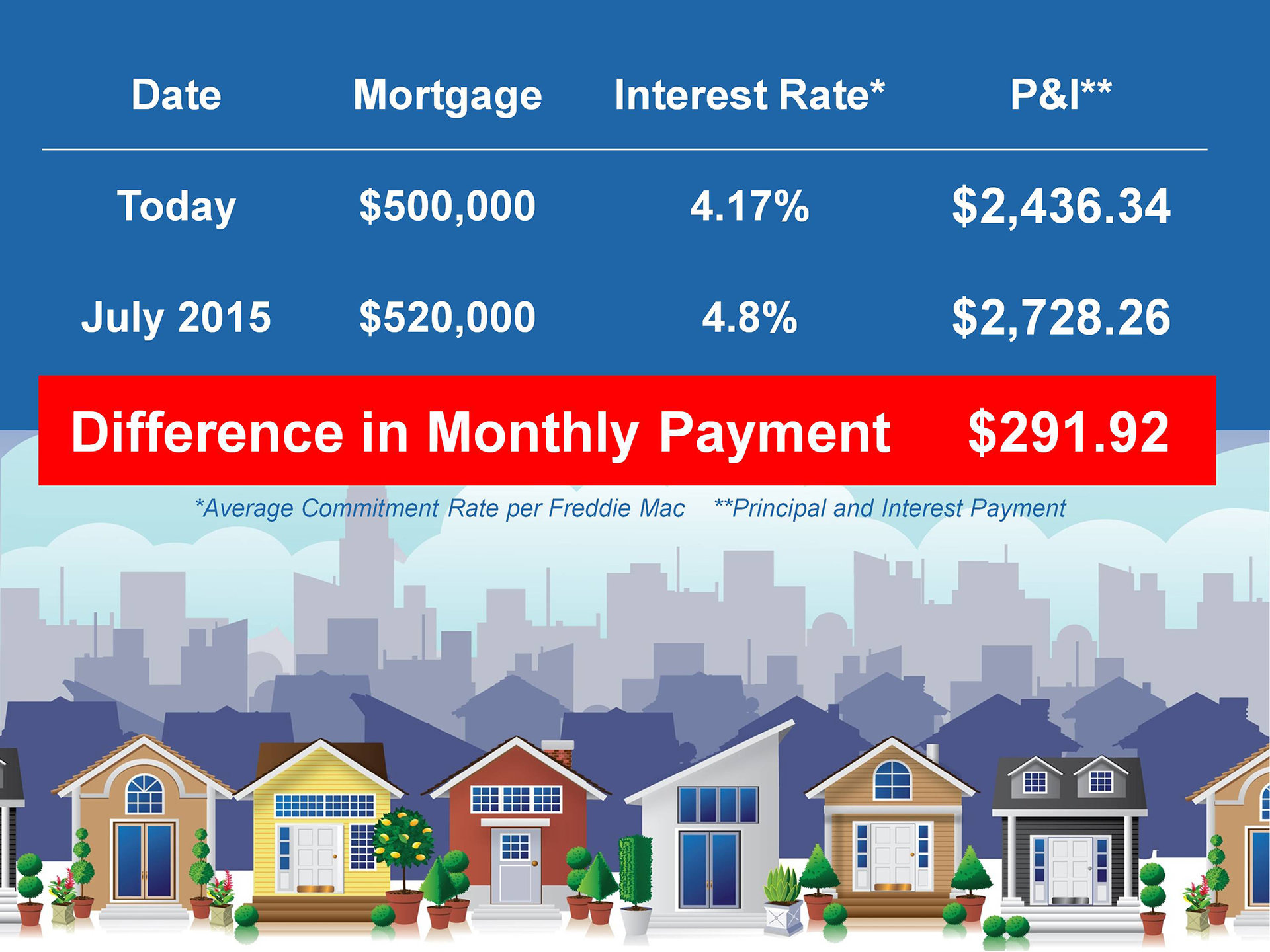

Raising Rates Affect the Cost, Too

Mortgage rates have risen 0.5% in 2018 on 30-year and 15-year fixed rate mortgages and experts expect them to continue to increase. Buyers paying attention to the market understand the relationship that inventory has on pricing; when the supply is low, the price usually goes up. Rising interest rates can affect the cost of homes also.

Mortgage rates have risen 0.5% in 2018 on 30-year and 15-year fixed rate mortgages and experts expect them to continue to increase. Buyers paying attention to the market understand the relationship that inventory has on pricing; when the supply is low, the price usually goes up. Rising interest rates can affect the cost of homes also.

When interest rates go up, fewer people can afford homes. Lower numbers of buyers can affect the demand, which could cause prices of homes to come down. The question is how much do the interest rates have to go up to affect demand?

As the rates gradually go up, the affect may not be noticeable at all except for the fact that the payments for the buyer have increased.

A ½% change in interest is approximately equal to a 5% change in price. A $300,000 mortgage at 4.5% for a 30-year term will have a $1,520.06 principal and interest payment. If the mortgage rate goes up 0.5%, it would affect the payment the same as if the price had gone up 5%. The difference in payments for the full term of the loan would be $32,547.

There are some things beyond buyers’ control, but indecision isn’t one of them. If they haven’t found the “right” home yet, it is understandable. However, when that home does present itself, the buyer needs to be ready to make a decision. If they are preapproved and have done their due diligence in the market, they should be able to contract before significant changes occur in the mortgage rates.