FHA MIP Release

FHA MIP Release

FHA loans require mortgage insurance premium to cover a possible loss to the lender if the property has to be foreclosed and sold. The premium is substantial and eliminating the MIP would reduce the payment considerably.

|

|

The MIP must remain in effect for five years but after that, when the balance is 78% of the original purchase price, FHA will release the requirement and your monthly payment will go down. Since amortization is affected by interest rates, the normal time to reach this 78% point could be from 9 to 12 years at today's interest rates.

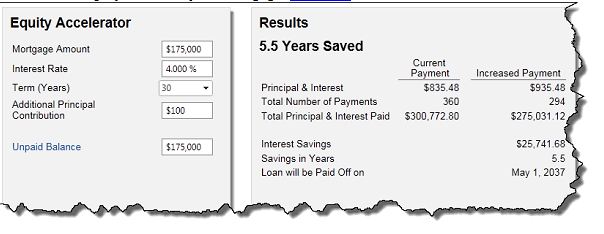

In the example below, the MIP would be released in 9 years 6 months with normal payments. An extra $100 a month would allow the borrower to reach the release point in 7 years 1 month. To reach the release point in the minimum five years, the borrower would have to make an extra $268.04 per month principal contribution.

Releasing the MIP in this example would save the borrower $177.67 per month. The borrower would also save interest, build equity and shorten the term of their mortgage. Once the MIP is released, the borrower could continue the same payment schedule to further accelerate the debt reduction.

To make some projections on your mortgage, click here.