Assumptions May Be an Alternative

For the last 25 years, most buyers have gotten a new mortgage or paid cash when purchasing a home. For a practical reason, owner-occupant buyers have another alternative: assuming a lower interest rate existing FHA or VA mortgage.

In the late 80’s, both FHA and VA began requiring buyers to qualify to assume their mortgages. Prior to that, good credit or even a job wasn’t required. The real reason there haven’t been significant numbers of assumptions in the past 25 years is that interest rates have been steadily going down. If a person had to qualify, they might as well do it on a new loan and get a lower interest rate.

Even though mortgage money is currently attractive and available, it is at a four-year high. When interest rates on new mortgages are higher than the rates of assumable FHA and VA mortgages originated in the recent past, it may be more advantageous to assume the existing mortgages. Conventional loans have due on sale clauses that prevent them from being assumed at the existing rate.

FHA loans that originated with lower than current interest rates have great advantages for buyers and sellers.

- Interest rate won't change for qualified buyer

- Lower interest rate means lower payments

- Lower closing costs than originating a new mortgage

- Easier to qualify for an assumption than a new loan

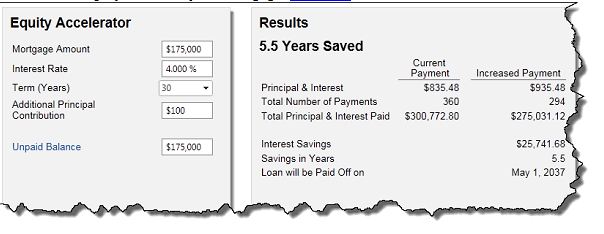

- Lower interest rate loans amortize faster than higher ones

- Equity grows faster because loan is further along the amortization schedule

- Assumable mortgage could make the home more marketable

This financing alternative can save money for the buyer in closing costs and monthly payments. While the equity may be more than the down payment on a new mortgage, second mortgages are available to make up the difference. Call us at (859) 647-0700 to find out if this may be an option for you.