7 Reasons to Buy a Home

Some people don't need a reason to buy a home, they just want it. That can be enough justification by itself. Other people need some solid logic before they're ready to make the commitment. The following reasons might help you to make a decision.

- Pride of ownership ... among the most popular reasons given by homebuyers is that they want a place they can call their own and decorate and improve it the way they want. It is a place to feel safe and secure and a place for their family. They can share it with their friends and enjoy living in it.

- Good investment ... Homeowners have a 80 times greater net worth than renters. By investing in a home that appreciates over time, it contributes to an increasing equity. The high loan to value mortgages that are available combined with the low mortgage rates also contribute to the investment through leverage which has been described as "using other people's money" to control an investment.

- Interest and property tax deductibility ... Homeowners can deduct their qualified mortgage interest and up to a maximum of $10,000 of their property taxes as itemized deductions on their federal income tax return. In some instances, the standard deduction may benefit them more, but they can elect to choose either method each year, whichever helps them the most.

- Capital gain exclusion ... A single homeowner can exclude up to $250,000 of capital gain and if married filing jointly, can exclude up to $500,000 of gain on their principal residence. The need to have owned and occupied it as their home for two of the last five years.

- Cash out refinance ... Generally speaking, a lender will allow an owner with good credit and income to borrow the difference in their current unpaid balance and 80% of the fair market value. This money can be used for any purpose and is not a taxable event.

- Equity buildup ...The difference in the value of the home and the unpaid mortgage balance is called equity and it increases with each payment made. It is like automatic savings.

- No landlords ... Instead of dealing with landlords who may impose restrictions on things like painting, improvements and pets. Owners are not concerned about rent increases and will have a fixed principal and interest payment for as long as they have a mortgage.

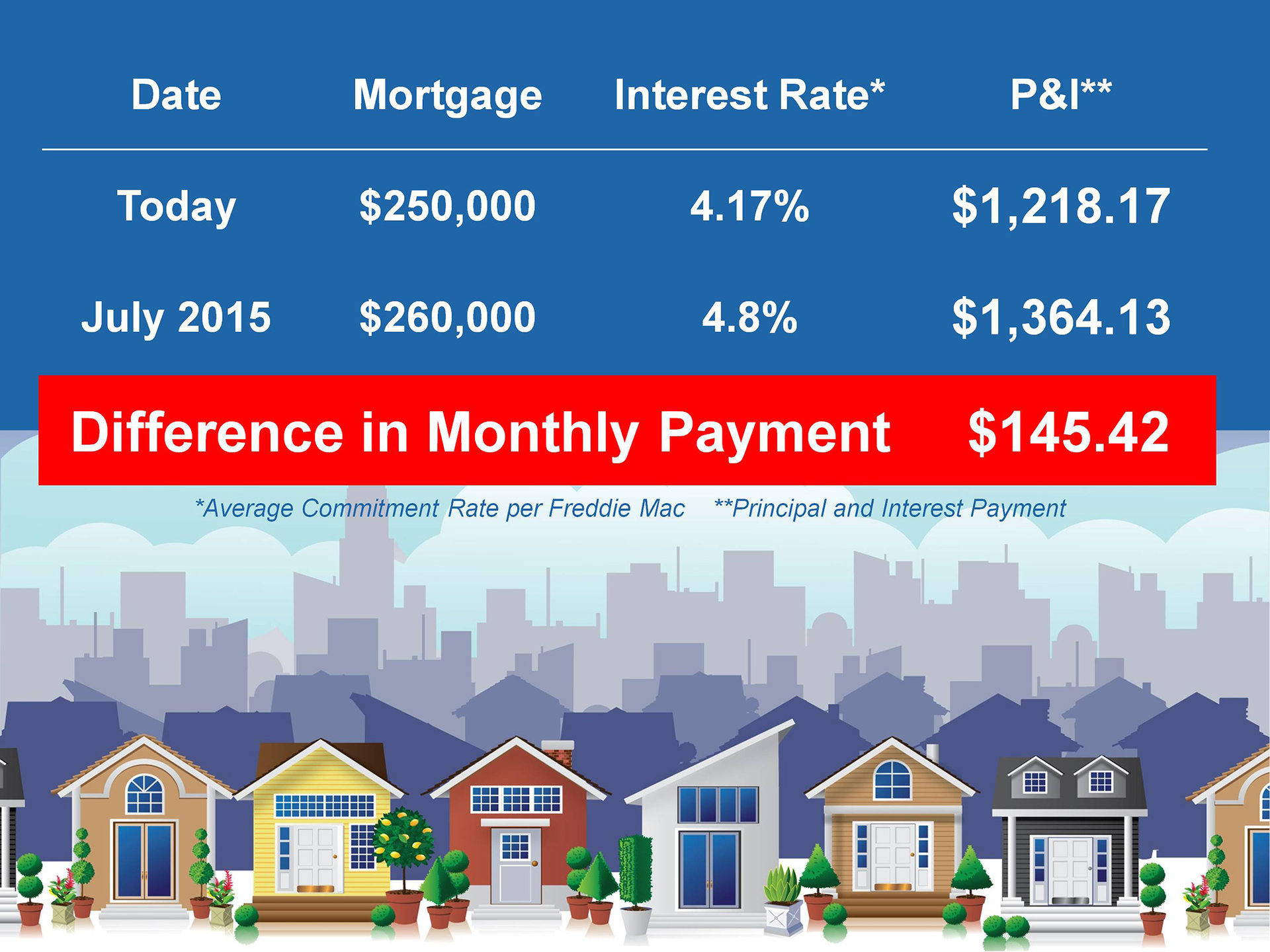

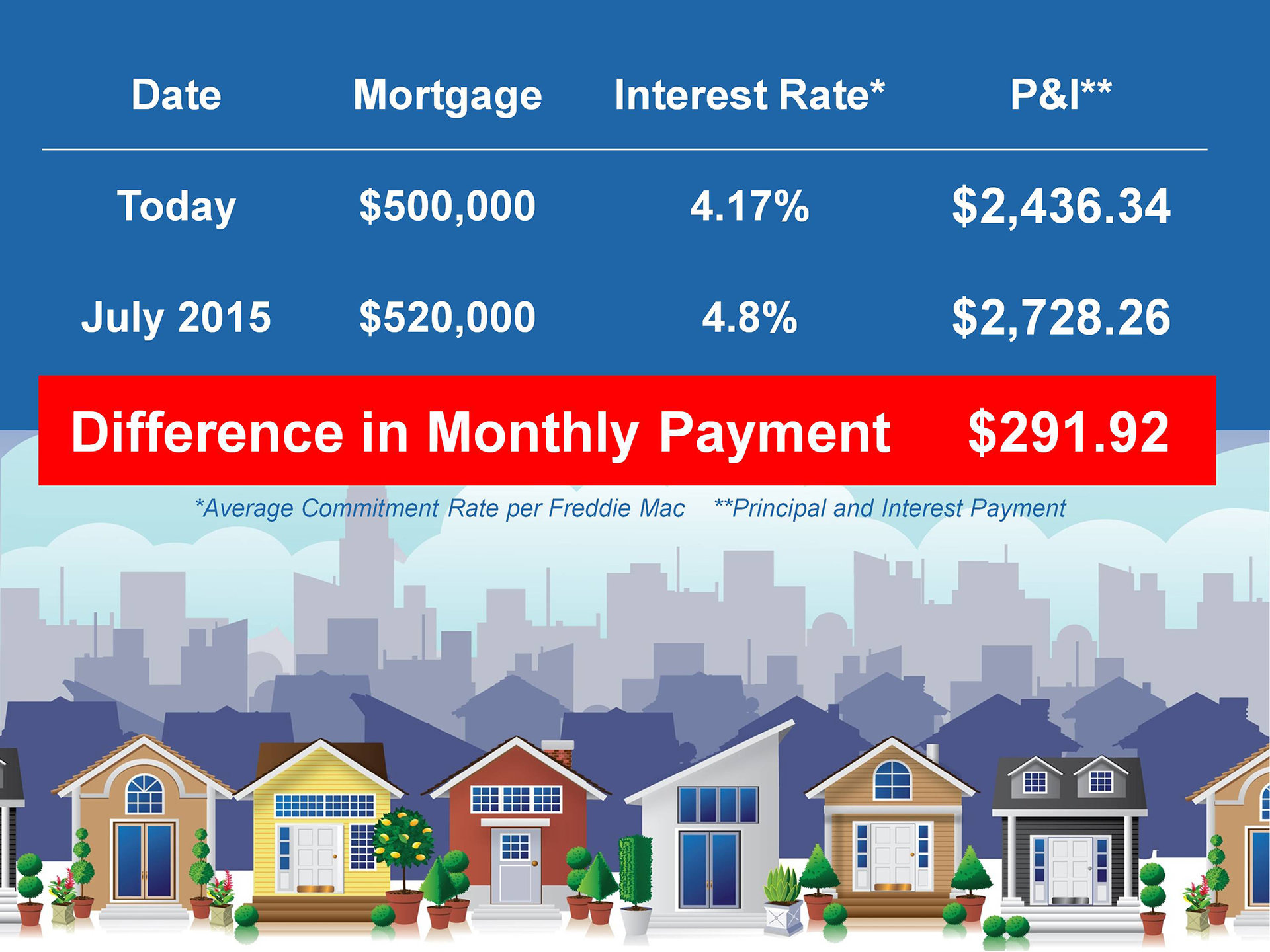

A bonus reason to buy a home now are the low mortgage rates available. The lowest rate recorded by Freddie Mac is 3.35% in December 2012. Today's rates are 3.75% on a 30-year fixed rate mortgage and 3.21% on a 15-year fixed rate mortgage. So, they are certainly very close to all-time lows.

The highest rate on a 30-year fixed rate mortgage was 18.45% in October 1981. When you put today's rates in perspective, they are an incredible bargain. Many industry experts expect that they will not remain as low as they are now. Locking in a low rate can keep your housing costs low.

A $275,000 mortgage at 3.75% for 30 years has a principal and interest payment of $1,273.57. If the rate goes up by 1%, the payment would increase to $1,434.53 or $160.96 per month for the 30-year term. Check the Rent vs. Own to see how the numbers look in your situation.